Modern Credit Strategy for Gen Z

"A credit score is not a number about the past. It is a number about who you can become - it determines whether you can rent the flat, get the mortgage, or qualify for the car loan."

Here's the uncomfortable truth that BNPL marketing does not mention: credit cards, used strategically, remain the single most powerful financial tool available to a young person building their future. The key word is strategically.

Paying your balance in full each month costs you exactly zero in interest while building a credit history that unlocks homeownership, better insurance premiums, and lower borrowing costs for life. The 24-49% APR figure that terrifies Gen Z applies only to revolving balances - money you have not paid back. If you treat a credit card exactly like a debit card (only spend what you have) and pay in full, the APR is irrelevant. What remains are: rewards, fraud protection, and credit building.

Rewards optimisation matters more than many Gen Z consumers realise. Cards aligned with this generation's lifestyle - high cashback on food delivery, streaming, travel, and rideshares - effectively reduce the cost of everyday spending by 1.5-5%. Over a year of ordinary purchases, this compounds meaningfully.

Fraud and purchase protection remains the most underappreciated credit card benefit. Disputed a fraudulent BNPL charge lately? It can take weeks. Disputing a credit card charge? Federal law requires a response within 30 days and often results in immediate provisional credit. If you buy a laptop that arrives broken, your credit card's purchase protection can reimburse you. BNPL offers no equivalent.

Major banks are paying attention. American Express, JPMorgan Chase, and Citi have all launched card-based BNPL instalment plans embedded within credit accounts. These hybrid products offer the flexibility Gen Z wants while preserving the consumer protections and credit-building benefits of traditional credit. It is, in many ways, the best of both worlds.

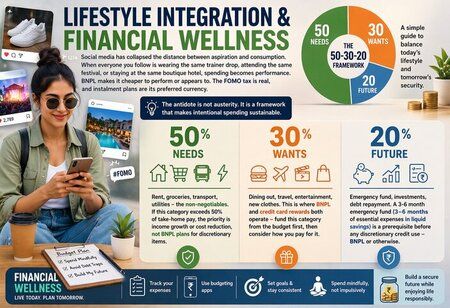

Lifestyle Integration & Financial Wellness

Social media has collapsed the distance between aspiration and consumption. When everyone you follow is wearing the same trainer drop, attending the same festival, or staying at the same boutique hotel, spending becomes performance. BNPL makes it cheaper to perform or appears to. The FOMO tax is real, and instalment plans are its preferred currency.

The antidote is not austerity. It is a framework that makes intentional spending sustainable.

50% Needs

Rent, groceries, transport, utilities - the non-negotiables. If this category exceeds 50% of take-home pay, the priority is income growth or cost reduction, not BNPL plans for discretionary items.

30% Wants

Dining out, travel, entertainment, new clothes. This is where BNPL and credit card rewards both operate - fund this category from the budget first, then consider how you pay for it.

20% Future

Emergency fund, investments, debt repayment. A 3-6 month emergency fund (3–6 months of essential expenses in liquid savings) is a prerequisite before any discretionary credit use - BNPL or otherwise.

Top-rated tools for Gen Z financial management in 2026 include: CRED (credit card management, India), Fi Money (smart banking with spending analytics), Copilot (US, AI-powered budgeting), and Mint alternatives like Monarch Money for comprehensive net worth tracking. For BNPL users specifically, apps that aggregate all active instalment plans into a single view - showing true total obligations - are increasingly essential.