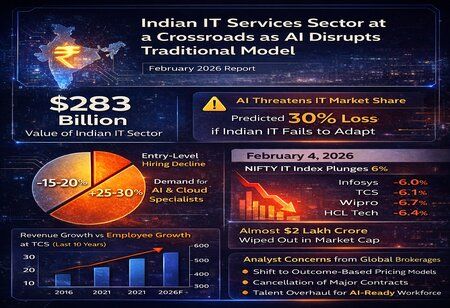

The Indian IT services sector is in a historic crossroads with a value of 283 billion dollars. Over the decades it has been built on a very basic, potent formula, lots of engineers, cost arbitrage and readiness to accept the technological grunt work of the world. However, with the coming of age of artificial intelligence beyond a buzzword to a real productivity engine, this formula is now being given a trial in ways it has never been. The question that has been plaguing the boardrooms is no longer whether AI will transform Indian IT, but whether the industry is going to be able to endure the disruption it has helped create.

Where AI Hits Hardest

The Indian IT business model has been based on the time and material (T&M) pricing model where the clients pay per hour instead of the deliverables. This model was a motivation to Indian companies to increase the number of employees instead of their output. Revenues have increased by a factor of two at TCS, an increase of USD 15 billion to 30 billion in the last ten years, although the number of headcount has increased nearly twice, to 608,000 employees, meaning that revenue per employee has not grown, and now hovers around 49,000. This is not a sign of efficiency; it is a structural vulnerability.

AI-powered tools are now capable of automating large swathes of entry-level IT work — code generation, software testing, data processing, documentation, and basic application support. Generative AI platforms can compress what once took a team of ten engineers several weeks into a matter of hours. According to industry analysts, experts predict that AI could lead to a 30% loss in market share for Indian IT if the sector fails to adapt. Entry-level hiring for legacy roles is already estimated to contract 15–20%, even as demand for advanced AI and cloud specialists rises 25–30%.

The timing is critical. Over the past few months, stock performance of large Indian IT firms has come under pressure as valuations reset following announcements from companies like Anthropic, whose AI tools threaten traditional application services delivery models.

The Stock Market Has Already Delivered Its Verdict

The financial markets have not yet given analysts time to argue about the long-term effects of AI, they are already pricing the disruption in with some brutal precision. The Nifty IT index on February 4, 2026 recorded the largest single day decline since March 2020, erasing almost Rs 2 lakh crore in market capitalization of the top IT firms of India in a single day. The trigger was not a weak earnings report or a macroeconomic shock- the immediate catalyst was the launch of a new AI automation system by Anthropic, whose expanded Claude "Cowork" agents were designed to automate tasks across legal, sales, marketing, and data roles- functions widely seen as core revenue drivers for IT services providers worldwide.

Infosys went down by 6 percent to a three-month low, TCS dropped down 6 percent intra day, Wipro lost 6.7 percent and HCL Tech lost 6.44 percent, as the entire Nifty IT index declined almost 6 percent with all its members recording losses. The slaughter did not end there- in the following weeks, Coforage and Infosys plunged down by nearly a quarter each, Persistent by a fifth, LTIM by a quarter, and TCS by an eighteenth, which took the Nifty IT index to a two-year low of its own bottom, and the Coforage and Infosys crashed by more than 19 percent on calendar year 2026 alone, compared to just 2 percent drop in the Nifty 50 index itself.

Commenting on the trillion-dollar market wipeout following Anthropic’s Claude agent launch, Ravi Kumar S, CEO, Cognizant described it in one word: “Overreaction. The market is pricing disruption faster than actual enterprise adoption. AI will transform service delivery, not eliminate service demand.”

The global brokerages jumped on it: Jefferies downgraded six large Indian IT firms saying that AI can fundamentally alter the structure of the IT business mix towards consulting and implementation and less managed services- more cyclical and that the talent and operating model would have to be overhauled. Citrini Research analysts went further to outline a conversation where cancelation of contracts at TCS, Infosys and Wipro might pick up speed, and JP Morgan cautioned that Indian IT companies might fail to satisfy expansion objectives as AI-driven gains encourage clients to shift budgets out of aggregate outsourcing. The market message is clear that the old Indian IT playing field is shattered and no one wants to pay top money on headcount-based, legacy-service companies in the era of smart automation.

Calling the market reaction excessive, Jensen Huang, CEO, NVIDIA remarked “The selloff triggered by Anthropic’s AI announcement is most illogical. AI does not destroy software — it dramatically accelerates its creation and value. The long-term opportunity for software and services is far bigger, not smaller.”

Also Read: Finance Outlook 2026: Markets, Policy and the Road Ahead

The Double-Edged Sword

AI is not an entirely negative phenomenon, and it is also a possible re-platform. Global capability centers (GCCs) are proliferating faster in India, with over 150 additional new GCCs having been launched over the past 30 months putting pressure on AI, cloud, and cybersecurity experts. Microsoft has allocated 3 billion dollars to invest in cloud and AI infrastructures in India in the year 2025, and Amazon Web Services developed Local Zones in Chennai, Hyderabad, Kolkata, and Pune. Such investments have the potential to create another cycle of high-value employment to the Indian IT professionals- though not to those who have not reskilled.

The response is being taken by some Indian firms. In 2023, Wipro introduced its ai360 program and committed 1 billion dollars to AI. Nevertheless, structural issues are still daunting. Having more than 60 percent employees at entry levels, the workforce reskilling challenge has colossal monetary weight - and cost.

What Needs to Change

The path forward for Indian IT is clear, even if it is not easy. Companies should not focus on the T&M model based on the number of people but on the outcome-based pricing model where the companies are rewarded on the basis of the results delivered rather than hours worked. They also need to invest in something that is meaningful regarding AI-native service capabilities, proprietary platforms, and domain-specific solutions which are not easily replicated using a generic AI tool.

The wage structures will have to be changed as well. The escalating GCC salaries, which are already 15-20 percent higher than those of traditional IT firms, are stealing the best talent off the legacy service providers. To retain AI-competent engineers will involve more than increased salaries, but more challenging and valuable work.

Addressing fears of job losses and margin pressure, Rajesh Gopinathan, Former CEO & MD, Tata Consultancy Services (TCS) stated, “AI will fundamentally reshape delivery models, but it will expand the scope of services, not shrink it. Indian IT firms that invest aggressively in reskilling and platforms will emerge stronger from this transition.”

The Verdict

The Indian IT industry is not becoming extinct - but is experiencing a radical re-inventing. The industry is no longer based on the low-margin, high-volume labor model. Companies that transform into AI-first, result-oriented businesses will have a substantial portion of what Bessemer Venture Partners a 400 billion Indian IT sector may become by 2030. The ones that are holding on to the old playbook will see their market share drop not in decades, but in years.

To the investors, the communication is also very clear the winners in Indian IT in the next generation will not resemble the giants of today. The companies to follow are not the ones with the most number of heads, but the ones that are the fastest to be intelligent in their automation, IP development and results delivery. In the age of AI, size is no longer a moat. Adaptability is.

On AI’s long-term role in Indian IT, Salil Parekh, CEO & MD, Infosys stated, “Generative AI is a massive productivity multiplier. Our focus is on building AI-first capabilities that help clients grow faster, operate leaner, and innovate continuously, while creating new high-value roles for our workforce.”