Decoding the New Labour Codes: A Double-Edged Sword for Women?

India's Landmark consolidation of 44 central labour laws into four broad Labour Codes on Wages, Industrial Relations, Social Security, and Occupational Safety by India stands as the most significant reform in the labour framework in decades. However, the effect of India’s new Labour Codes 2026 on female take-home salary has both positive and negative aspects.

The most significant provision for working women is the 50% Wage Rule in the Code on Wages. This provision stipulates that allowances must not form 50% of an employee’s remuneration, thereby boosting the basic wage component. This sounds like unambiguous good news on the surface. A higher basic wage means larger contributions to the Employees’ Provident Fund (EPF) and higher gratuity payouts – critical long-term wealth-building tools, especially for women, who suffer more career breaks than men due to greater caregiving responsibilities.

Also Read: India's New Labor Codes 2026: Impact on Salary, PF, and Work Culture

The short-term take-home pay effect of 2026 Labour Codes, on the other hand, offers a genuine financial planning challenge. If a woman currently enjoys a large chunk of her compensation in the form of allowances – House Rent Allowance, Leave Travel Concession, special allowances, a restructured salary to comply with the 50% basic wage rule means she and her employer remit higher contributions to EPF every month. This will improve her retirement prospects but will lower the monthly net salary that goes to her bank account.

This is not a reason for opposing the reform. On the contrary, it is a call for financial literacy. This is not a reason to oppose the reform but a call for financial literacy; Financial advisors and HR teams must communicate these changes in no uncertain terms, more so when the organization has a significant number of female employees in IT services, healthcare, and FMCG retail.

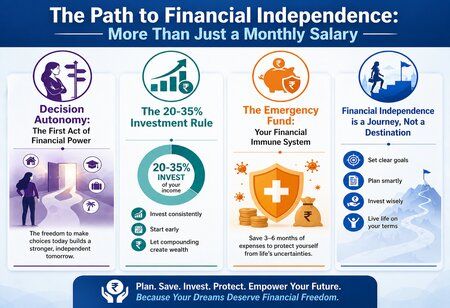

The Path to Financial Independence: More Than Just a Monthly Salary

Earning a salary is the foundation of financial independence for the modern Indian woman - but it is emphatically not the whole structure. A financial independence guide for Indian women in 2026 must address the gap between earning money and controlling it, between receiving a wage and building lasting wealth.

Decision Autonomy: The First Act of Financial Power

In a significant proportion of Indian households, women who earn salaries still defer major financial decisions to male family members - husbands, fathers, or brothers. This is not merely a cultural observation; it is an economic vulnerability. A woman who earns but does not decide remains financially dependent in all the ways that matter when life takes unexpected turns: divorce, widowhood, illness, or job loss. Decision autonomy - the right and practice of making one's own investment, insurance, and savings decisions - is the first and non-negotiable pillar of genuine financial independence.

The 20-35% Investment Rule

Investment strategies for working women in India must move beyond the safety of Fixed Deposits, which currently offer returns that barely outpace inflation. Financial planners broadly recommend that working women invest between 20% and 35% of their monthly net income into growth instruments. For those beginning their journey, a Systematic Investment Plan (SIP) in a diversified equity mutual fund offers the dual advantages of rupee cost averaging and the power of compounding. A woman earning Rs 40,000 per month who consistently invests Rs 8,000 monthly in a diversified fund at a moderate 12% annual return can accumulate approximately Rs 1.86 crore over 25 years - a sum no Fixed Deposit strategy can meaningfully replicate.

The Emergency Fund: Your Financial Immune System

Before any aggressive investment begins, every working woman should build an emergency fund equivalent to six months of her total monthly expenses. This fund - kept in a liquid savings account or a short-duration liquid mutual fund — is not an investment but an insurance policy against life's disruptions: a career change, a medical emergency, a need to support family, or the courage required to leave an unfulfilling job. The emergency fund transforms financial choices from desperate reactions into deliberate decisions.